金融数据分析库yfinance,初次使用体验!

原创

金融数据分析库yfinance,初次使用体验!

原创

皮大大

发布于 2023-08-29 00:20:56

发布于 2023-08-29 00:20:56

公众号:尤而小屋 作者:Peter 编辑:Peter

大家好,我是Peter~

今天给大家介绍一个金融数据分析库yfinance,主要是基于该库下的股票数据分析及股价预测(使用LSTM模型)

yfinance库

yfinance 是一个用于从 Yahoo Finance 获取金融数据的 Python 库。它提供了一个方便的接口,让用户能够轻松地下载和处理股票、指数、货币对等金融市场的历史价格数据和其他相关信息。yfinance 让开发者和分析师能够使用 Python 进行金融数据分析、可视化和研究。

以下是 yfinance 的一些特点和功能:

- 简单易用的接口: yfinance 提供了简单的函数调用,使用户能够通过指定股票代码、日期范围等参数来获取历史价格数据。

- 多种数据获取: 除了股票价格数据,yfinance 还可以获取其他金融数据,如分红、拆股等。

- 多样的时间尺度: 用户可以选择不同的时间尺度,如日线、周线、月线等来获取不同粒度的数据。

- 数据处理和分析: 通过将数据转换为 pandas 数据框,用户可以方便地进行数据处理、计算技术指标和执行分析操作。

- 全球市场: yfinance 不仅仅支持美国市场,还能够获取许多全球市场的金融数据。

- 免费使用: yfinance 是一个免费开源的库,不需要额外的订阅费用。

使用方法:

1、安装pip install yfinance

2、获取股票数据

import yfinance as yf

# 指定股票代码

name = 'AAPL'

# 下载历史价格数据

apple = yf.download(name, start='2022-01-01', end='2022-12-31')导入库

In 1:

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

sns.set_style('whitegrid')

plt.style.use("fivethirtyeight")

%matplotlib inline

from datetime import datetime

# pip install pandas_datareader

from pandas_datareader.data import DataReader

import yfinance as yf

from pandas_datareader import data as pdr

yf.pdr_override()

import warnings

warnings.filterwarnings("ignore")下载数据

In 2:

# 获取4个公司股价信息

tech_list = ['AAPL', 'GOOG', 'MSFT', 'AMZN'] 设置股票的起止时间:

- 结束时间是现在

- 开始时间是过去一年

In 3:

end = datetime.now()

start = datetime(end.year - 1, end.month, end.day)基于yfinance库下载股票的数据:

In 4:

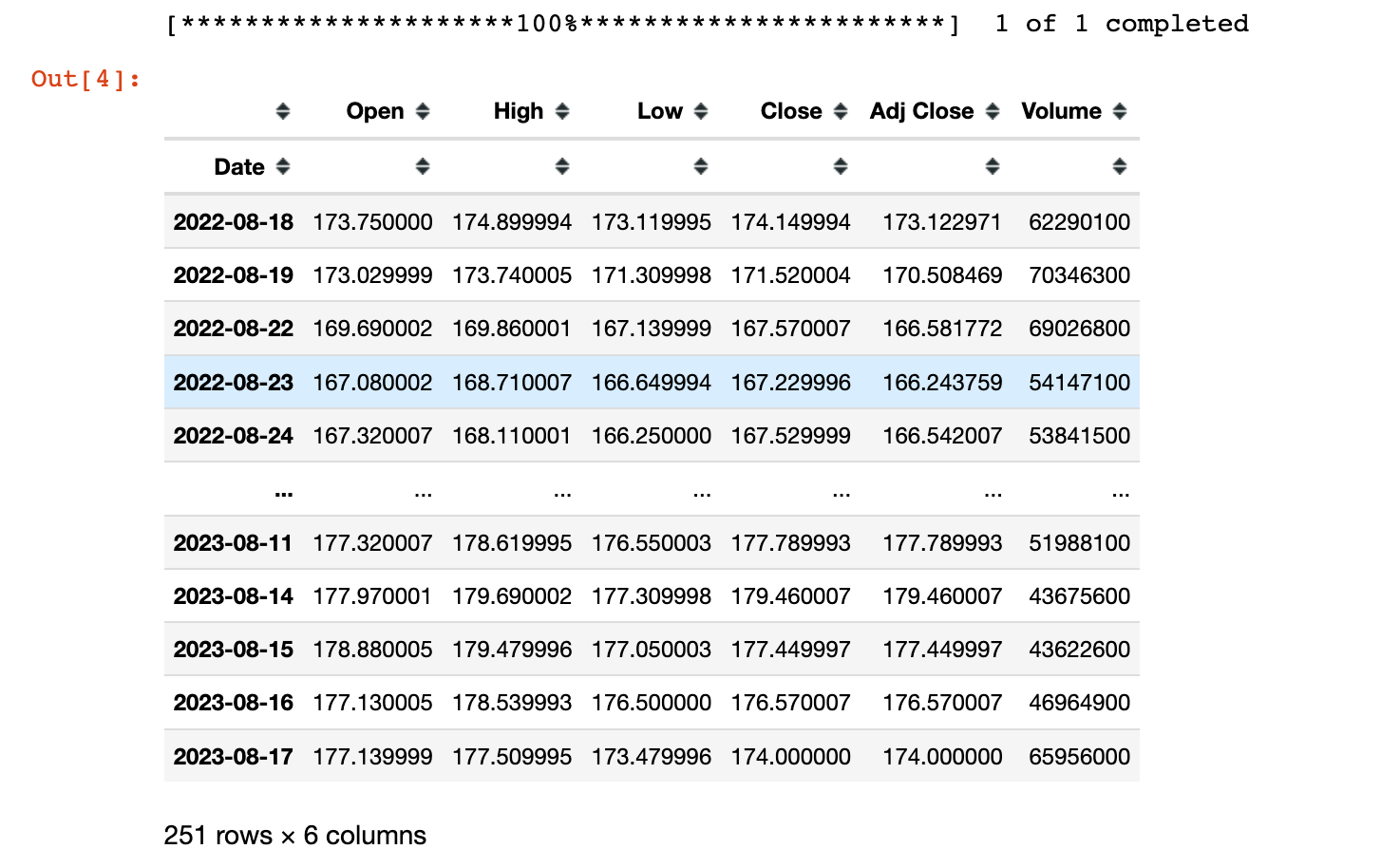

# 单个股票数据下载

yf.download("AAPL", start, end)

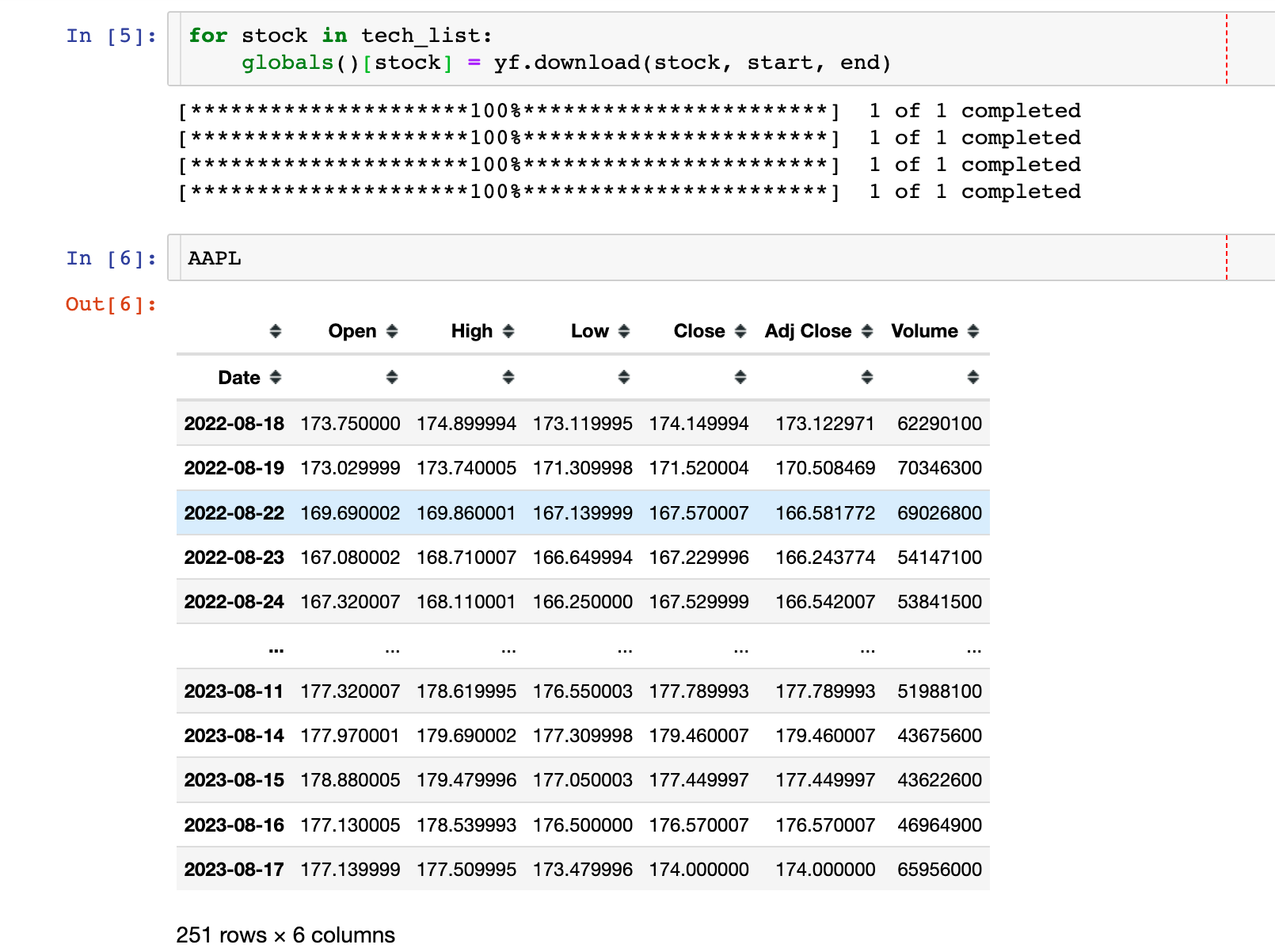

下面是循环遍历tech_list列表,将每个股票下载的数据(DataFrame)保存到对应的股票名字中:

In 5:

for stock in tech_list:

globals()[stock] = yf.download(stock, start, end)

[*********************100%***********************] 1 of 1 completed

[*********************100%***********************] 1 of 1 completed

[*********************100%***********************] 1 of 1 completed

[*********************100%***********************] 1 of 1 completed

公司名称和数据的配对:

In 7:

company_list = [AAPL, GOOG, MSFT, AMZN] # 上面下载的4个数据

company_name = ["APPLE", "GOOGLE", "MICROSOFT", "AMAZON"]

for company, com_name in zip(company_list, company_name):

# company 是每个股票的DataFrame数据

company["company_name"] = com_name此时,每个股票company作为全局变量已经更新,添加了新的字段company_name。

4个数据的合并:

In 8:

df = pd.concat(company_list, axis=0)

df.tail()

数据统计信息

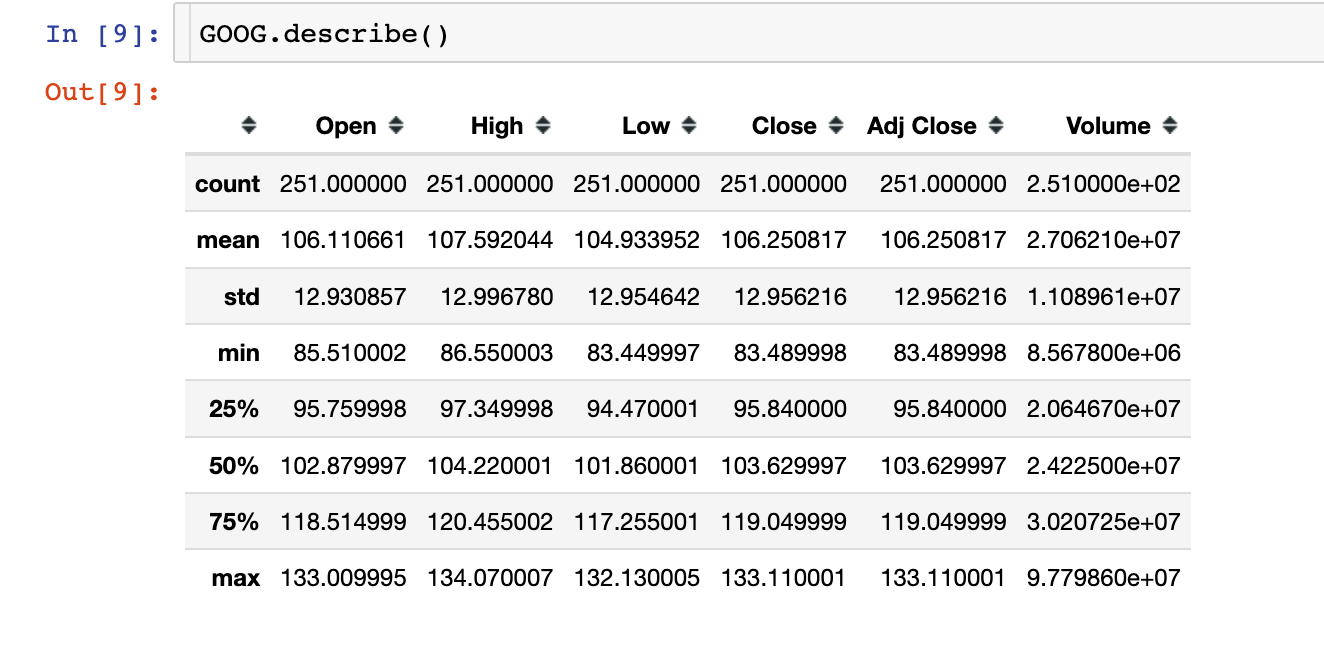

In 9:

GOOG.describe()Out9:

具体的数据信息,以谷歌股价为例:

In 10:

GOOG.info()

<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 251 entries, 2022-08-18 to 2023-08-17

Data columns (total 7 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Open 251 non-null float64

1 High 251 non-null float64

2 Low 251 non-null float64

3 Close 251 non-null float64

4 Adj Close 251 non-null float64

5 Volume 251 non-null int64

6 company_name 251 non-null object

dtypes: float64(5), int64(1), object(1)

memory usage: 15.7+ KB数据探索分析

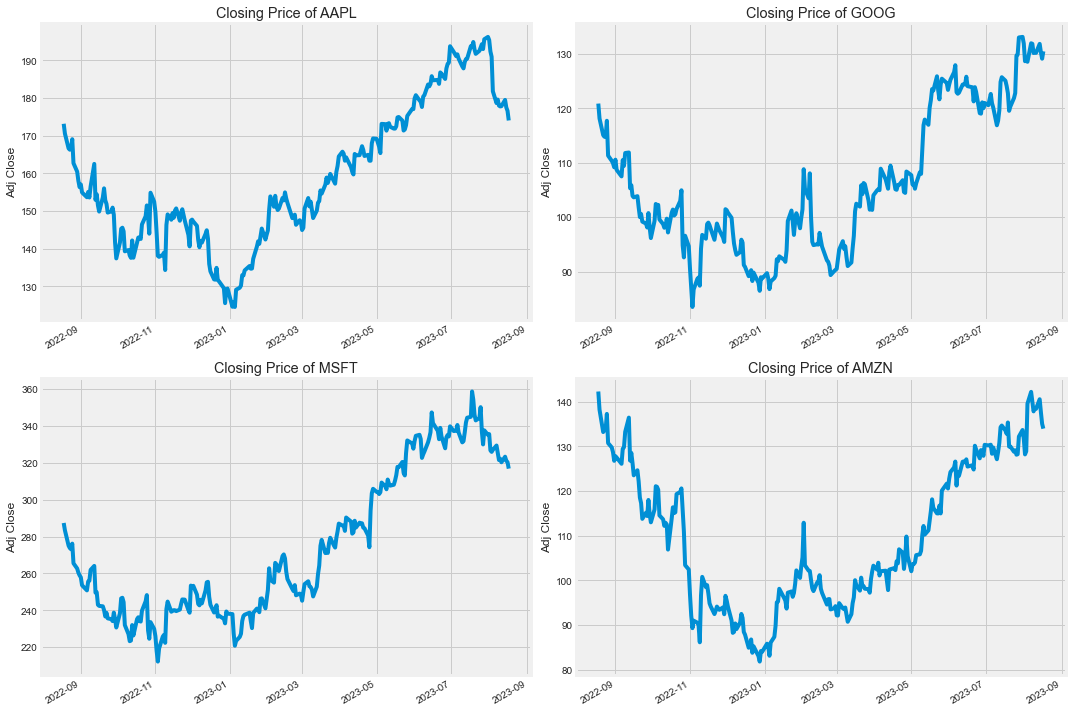

收盘价

In 11:

plt.figure(figsize=(15,10))

plt.subplots_adjust(top=1.25, bottom=1.2)

for i, company in enumerate(company_list, 1):

plt.subplot(2,2,i)

company["Adj Close"].plot()

plt.ylabel("Adj Close")

plt.xlabel(None)

plt.title(f"Closing Price of {tech_list[i-1]}")

plt.tight_layout()

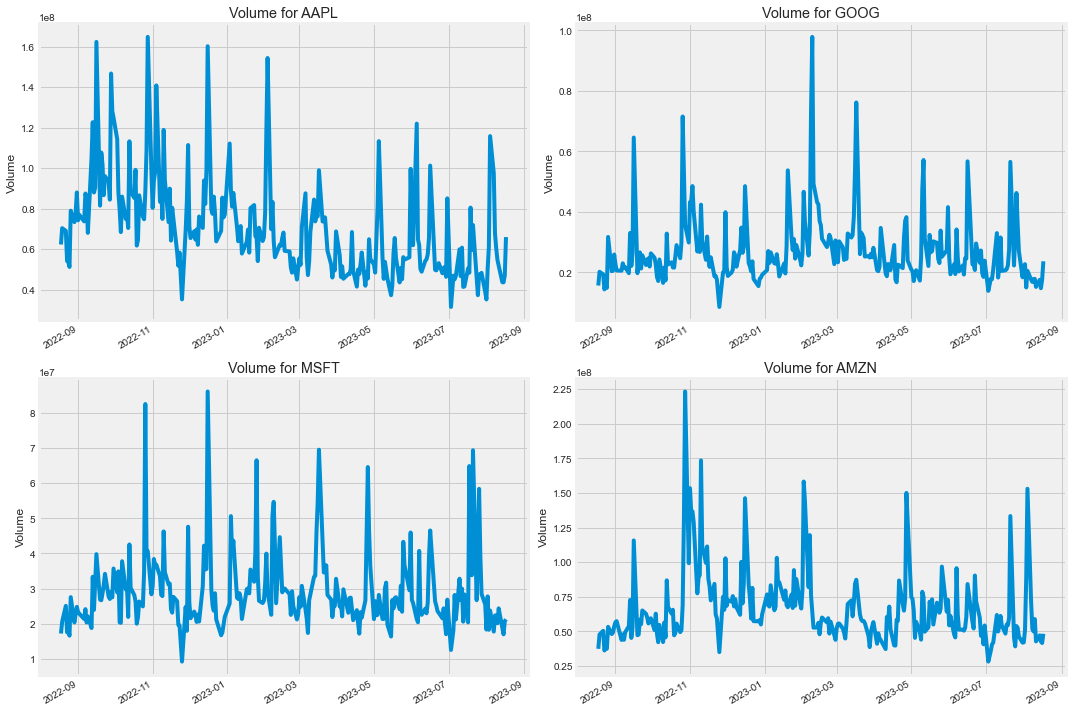

成交量对比

In 12:

plt.figure(figsize=(15,10))

plt.subplots_adjust(top=1.25, bottom=1.2)

for i, company in enumerate(company_list, 1):

plt.subplot(2,2,i)

company["Volume"].plot()

plt.ylabel("Volume")

plt.xlabel(None)

plt.title(f"Volume for {tech_list[i-1]}")

plt.tight_layout()

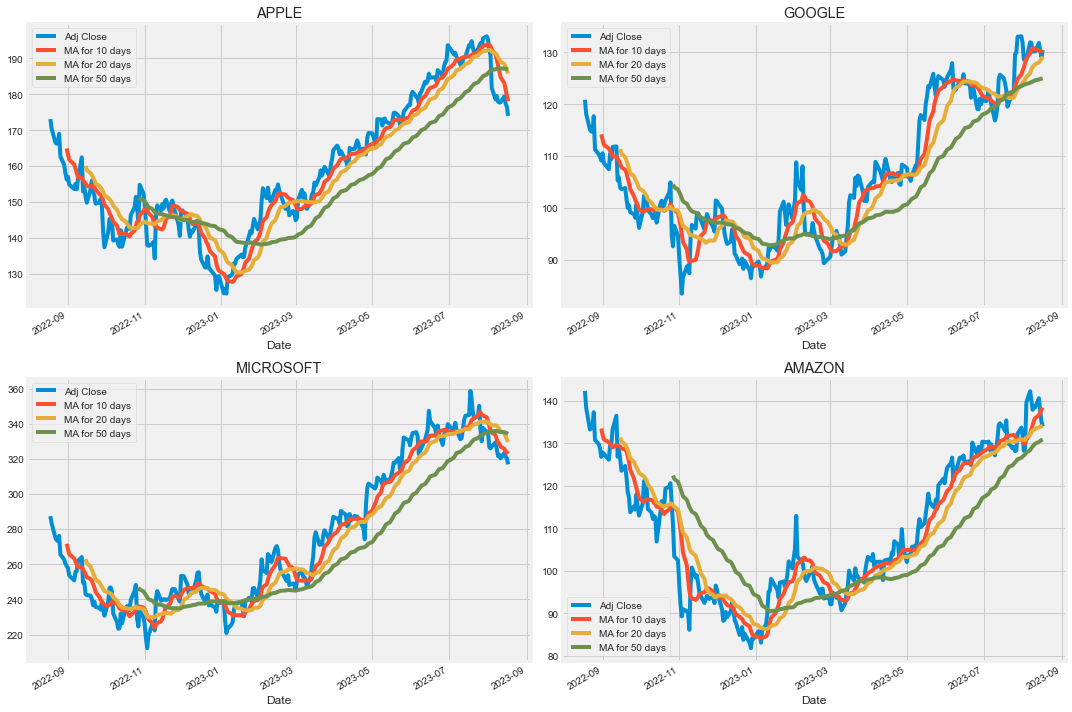

滑动平均

股票收盘价的滑动平均:

In 13:

ma_day = [10,20,50]

for ma in ma_day:

for company in company_list:

column_name = f"MA for {ma} days"

company[column_name] = company["Adj Close"].rolling(ma).mean()

fig, axes = plt.subplots(nrows=2, ncols=2)

fig.set_figheight(10)

fig.set_figwidth(15)

# 取出4个字段的数据进行绘图

AAPL[['Adj Close', 'MA for 10 days', 'MA for 20 days', 'MA for 50 days']].plot(ax=axes[0,0])

axes[0,0].set_title('APPLE')

GOOG[['Adj Close', 'MA for 10 days', 'MA for 20 days', 'MA for 50 days']].plot(ax=axes[0,1])

axes[0,1].set_title('GOOGLE')

MSFT[['Adj Close', 'MA for 10 days', 'MA for 20 days', 'MA for 50 days']].plot(ax=axes[1,0])

axes[1,0].set_title('MICROSOFT')

AMZN[['Adj Close', 'MA for 10 days', 'MA for 20 days', 'MA for 50 days']].plot(ax=axes[1,1])

axes[1,1].set_title('AMAZON')

fig.tight_layout()

可以看到模拟效果最好的是20日移动平均曲线

日回报率

使用Pandas中的pct_change函数:

具体来说,pct_change() 函数的功能是计算相邻元素之间的变化率,这在分析时间序列数据时非常有用。

该函数会将当前元素与前一个元素进行比较,并计算两者之间的百分比变化。这可以帮助分析者理解数据的波动情况,尤其是在金融分析等领域。

In 14:

for company in company_list:

company["Daily Return"] = company["Adj Close"].pct_change()In 15:

fig,axes = plt.subplots(nrows=2, ncols=2)

fig.set_figheight(10)

fig.set_figwidth(15)

AAPL["Daily Return"].plot(ax=axes[0,0],legend=True,linestyle="--",marker="o")

axes[0,1].set_title("APPLE")

GOOG['Daily Return'].plot(ax=axes[0,1], legend=True, linestyle='--', marker='o')

axes[0,1].set_title('GOOGLE')

MSFT['Daily Return'].plot(ax=axes[1,0], legend=True, linestyle='--', marker='o')

axes[1,0].set_title('MICROSOFT')

AMZN['Daily Return'].plot(ax=axes[1,1], legend=True, linestyle='--', marker='o')

axes[1,1].set_title('AMAZON')

fig.tight_layout()

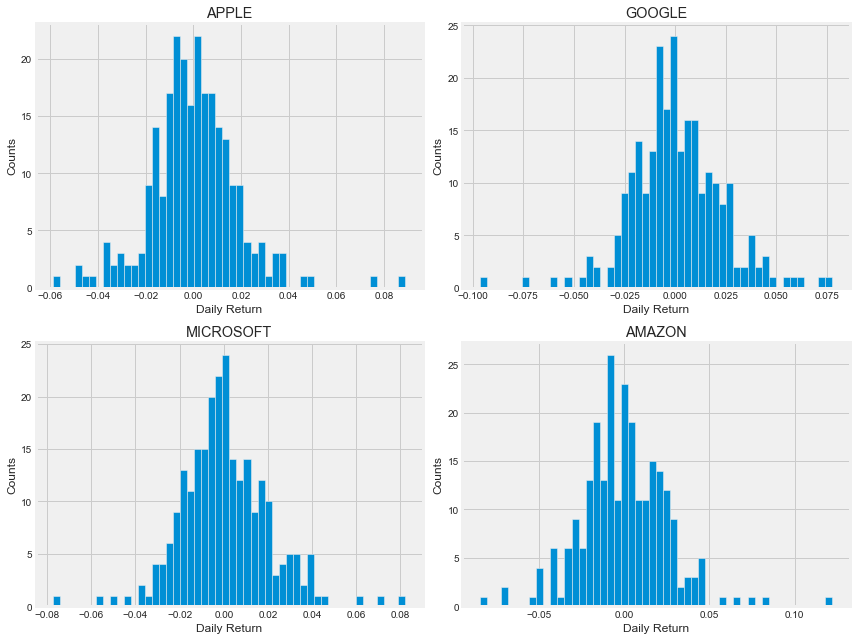

基于直方图和核密度图查看平均日回报率:

In 16:

plt.figure(figsize=(12,9))

for i, company in enumerate(company_list, 1):

plt.subplot(2,2,i)

company['Daily Return'].hist(bins=50)

plt.xlabel('Daily Return')

plt.ylabel('Counts')

plt.title(f'{company_name[i - 1]}')

plt.tight_layout()

相关性分析

不同股票回报率的相关性分析:

In 17:

from pandas_datareader import data as pdr

closing_df = pdr.get_data_yahoo(tech_list, start=start, end=end)["Adj Close"]

closing_df.head()tech_rets = closing_df.pct_change()

tech_rets.head()两两分布图

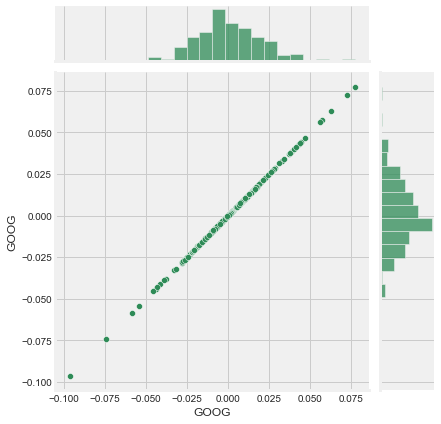

In 19:

# 自相关

sns.jointplot(x='GOOG',

y='GOOG',

data=tech_rets,

kind='scatter',

color='seagreen')

plt.show()

# 互相关

sns.jointplot(x='GOOG',

y='AAPL',

data=tech_rets,

kind='scatter')

plt.show()sns.jointplot(x='GOOG',

y='MSFT',

data=tech_rets,

kind='scatter'

)

plt.show()4个股票之间的相关性分析:

In 22:

sns.pairplot(tech_rets, kind='reg')

plt.show()

我们以谷歌和亚马逊的股票价格为例:

In 23:

# tech_rets = closing_df.pct_change() 回报率

return_fig = sns.PairGrid(tech_rets.dropna())

# 上下对角线绘制不同图形:上-散点图 下-kde密度图

return_fig.map_upper(plt.scatter, color='purple')

return_fig.map_lower(sns.kdeplot, cmap='cool_d')

# 主对角线:直方图

return_fig.map_diag(plt.hist, bins=30)

# closing_df = pdr.get_data_yahoo(tech_list, start=start, end=end)["Adj Close"]

returns_fig = sns.PairGrid(closing_df)

returns_fig.map_upper(plt.scatter,color='purple')

returns_fig.map_lower(sns.kdeplot,cmap='cool_d')

returns_fig.map_diag(plt.hist,bins=30)

plt.show()

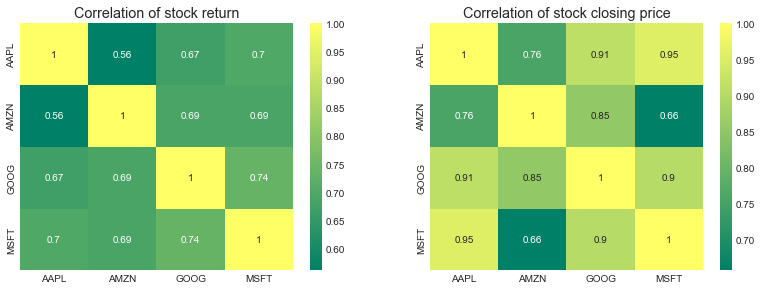

相关系数热力图

In 25:

plt.figure(figsize=(12, 10))

plt.subplot(2, 2, 1)

sns.heatmap(tech_rets.corr(), annot=True, cmap='summer')

plt.title('Correlation of stock return')

# 回报率

plt.subplot(2, 2, 2)

sns.heatmap(closing_df.corr(), annot=True, cmap='summer')

plt.title('Correlation of stock closing price')

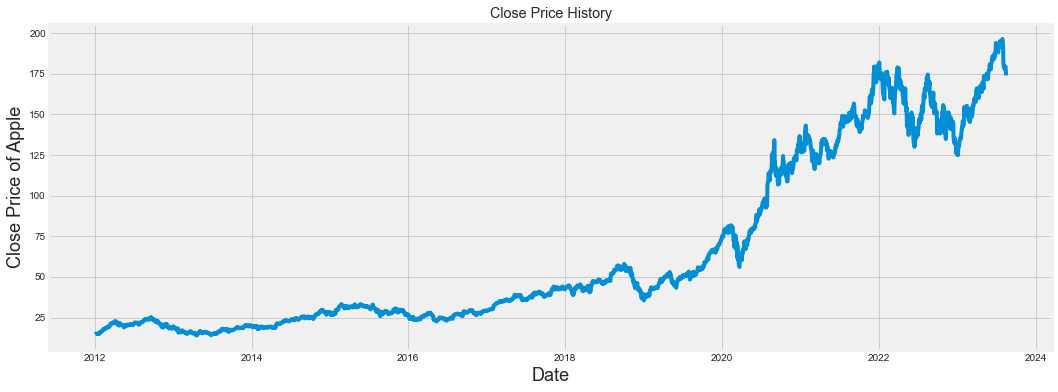

基于LSTM股价预测(APPLE为例)

获取数据

In 26:

df = pdr.get_data_yahoo('AAPL',

start='2012-01-01',

end=datetime.now()

)

df.head()收盘价的历史走势趋势图:

In 27:

plt.figure(figsize=(16,6))

plt.title('Close Price History')

plt.plot(df['Close'])

plt.xlabel('Date', fontsize=18)

plt.ylabel('Close Price of Apple', fontsize=18)

plt.show()

数据标准化

In 28:

data = df.filter(["Close"])

dataset = data.valuesIn 29:

from sklearn.preprocessing import MinMaxScaler

scaler = MinMaxScaler(feature_range=(0,1))

scaled_data = scaler.fit_transform(dataset) # 对整体数据的标准化

scaled_dataOut29:

array([[0.00405082],

[0.0044833 ],

[0.00538153],

...,

[0.89589184],

[0.89107004],

[0.876988 ]])数据切分

In 30:

training_data_len = int(np.ceil(len(dataset) * 0.95))

training_data_lenOut30:

2779In 31:

train_data = scaled_data[0:int(training_data_len), :]

x_train = []

y_train = []

for i in range(60, len(train_data)):

x_train.append(train_data[i-60:i, 0])

y_train.append(train_data[i, 0])训练集的shape重置:

In 32:

x_train, y_train = np.array(x_train), np.array(y_train)

x_train = np.reshape(x_train,(x_train.shape[0], x_train.shape[1], 1))

x_train.shapeOut32:

(2719, 60, 1)建模

In 33:

from keras.models import Sequential

from keras.layers import Dense, LSTM

# LSTM model

model = Sequential()

model.add(LSTM(128, return_sequences=True, input_shape= (x_train.shape[1], 1)))

model.add(LSTM(64, return_sequences=False))

model.add(Dense(25))

model.add(Dense(1))

model.compile(optimizer='adam', loss='mean_squared_error')训练模型

In 34:

model.fit(x_train, y_train, batch_size=1, epochs=1)

2719/2719 [==============================] - 168s 58ms/step - loss: 0.0013Out34:

<keras.callbacks.History at 0x15c3d2a10>模型预测

In 35:

test_data = scaled_data[training_data_len - 60: , :]

x_test = []

y_test = dataset[training_data_len:, :]

for i in range(60, len(test_data)):

x_test.append(test_data[i-60:i, 0])

x_test = np.array(x_test)In 36:

x_test = np.reshape(x_test, (x_test.shape[0], x_test.shape[1], 1 ))In 37:

# 模型预测

predictions = model.predict(x_test)

predictions = scaler.inverse_transform(predictions)

rmse = np.sqrt(np.mean(((predictions - y_test) ** 2)))

rmseOut37:

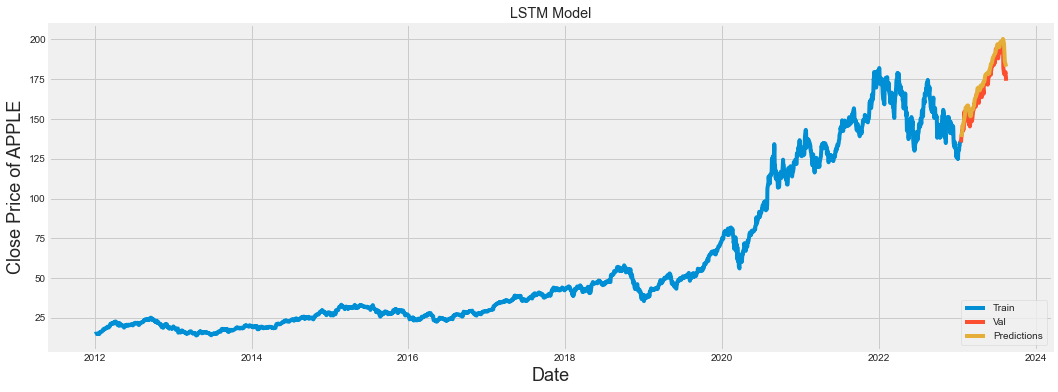

5.405450466807663预测结果可视化

In 38:

train = data[:training_data_len]

valid = data[training_data_len:]

valid['Predictions'] = predictions

plt.figure(figsize=(16,6))

plt.title('LSTM Model')

plt.xlabel('Date', fontsize=18)

plt.ylabel('Close Price of APPLE', fontsize=18)

plt.plot(train['Close'])

plt.plot(valid[['Close', 'Predictions']])

plt.legend(['Train', 'Val', 'Predictions'], loc='lower right')

plt.show()

原创声明:本文系作者授权腾讯云开发者社区发表,未经许可,不得转载。

如有侵权,请联系 cloudcommunity@tencent.com 删除。

目录

腾讯云开发者

Copyright © 2013 - 2026 Tencent Cloud. All Rights Reserved. 腾讯云 版权所有

深圳市腾讯计算机系统有限公司 ICP备案/许可证号:粤B2-20090059 ![]() 粤公网安备44030502008569号

粤公网安备44030502008569号

腾讯云计算(北京)有限责任公司 京ICP证150476号 | 京ICP备11018762号