尝试修改脚本ccxt python二进制点dca bot

尝试修改脚本ccxt python二进制点dca bot

提问于 2022-02-09 22:55:37

你好,我需要在二进制环境下修改dca bot的python脚本,我想修改在二进制上交易的原始脚本,我修改了exchange部分,但是当我尝试在visual studio中运行该脚本时,遇到了这个问题:

回溯(最近一次调用):文件"c:\Users\TEHH\Desktop\Binance-Futures-DCA-4Bot-main\Binance-Futures-DCA-Bot-main\strategy copy 2.py",第41行,位置=balance‘’info‘

你能帮我修改一下代码以便能在现场使用吗,

github ccxt:https://github.com/ccxt/ccxt.git

代码:

import config

import pandas as pd

import ccxt

import winsound

duration = 1000 # milliseconds

freq = 440 # Hz

# SETTİNGS

symbolName = input("Symbol (BTC, ETH, LTC...): ").upper()

baseOrderSize = float(input("Base Order Size: "))

safetyOrderSize = float(input("Safety Order Size: "))

maxSafetyTradesCount = float(input("Max Safety Trades Count: "))

priceDeviation = float(input("Price Deviation %: "))

safetyOrderStepScale = float(input("Safety Order Step Scale: "))

safetyOrderVolumeScale = float(input("Safety Order Volume Scale: "))

takeProfit = float(input("Take Profit %: "))

stopLoss = float(input("Stop Loss %: "))

positionSide = float(input("Position Side = Only Long(1) - Only Short(2) - Long and Short(3): "))

#ATTRIBUTES

first = True

tradeCount = 1

symbol = symbolName+"/BTC"

mainSafetyOrderSize = safetyOrderSize

mainPriceDeviation = priceDeviation

# API CONNECT

exchange = ccxt.binance({

"apiKey": config.apiKey,

"secret": config.secretKey,

'enableRateLimit': True

})

while True:

try:

balance = exchange.fetch_balance()

free_balance = exchange.fetch_free_balance()

positions = balance['info']['positions']

newSymbol = symbolName+"BTC"

current_positions = [position for position in positions if float(position['positionAmt']) != 0 and position['symbol'] == newSymbol]

position_info = pd.DataFrame(current_positions, columns=["symbol", "entryPrice", "unrealizedProfit", "isolatedWallet", "positionAmt", "positionSide"])

# in position?

if not position_info.empty and position_info["positionAmt"][len(position_info.index) - 1] != 0:

inPosition = True

else:

inPosition = False

longPosition = False

shortPosition = False

# in long position?

if not position_info.empty and float(position_info["positionAmt"][len(position_info.index) - 1]) > 0:

longPosition = True

shortPosition = False

# in short position?

if not position_info.empty and float(position_info["positionAmt"][len(position_info.index) - 1]) < 0:

shortPosition = True

longPosition = False

# LOAD BARS

bars = exchange.fetch_ohlcv(symbol, timeframe="1m", since = None, limit = 1)

df = pd.DataFrame(bars, columns=["timestamp", "open", "high", "low", "close", "volume"])

# Starting price

if first:

firstPrice = float(df["close"][len(df.index) - 1])

first = False

currentPrice = float(df["close"][len(df.index) - 1])

# LONG ENTER

def longEnter(alinacak_miktar):

order = exchange.create_market_buy_order(symbol, alinacak_miktar)

winsound.Beep(freq, duration)

# LONG EXIT

def longExit():

order = exchange.create_market_sell_order(symbol, float(position_info["positionAmt"][len(position_info.index) - 1]), {"reduceOnly": True})

winsound.Beep(freq, duration)

# SHORT ENTER

def shortEnter(alincak_miktar):

order = exchange.create_market_sell_order(symbol, alincak_miktar)

winsound.Beep(freq, duration)

# SHORT EXIT

def shortExit():

order = exchange.create_market_buy_order(symbol, (float(position_info["positionAmt"][len(position_info.index) - 1]) * -1), {"reduceOnly": True})

winsound.Beep(freq, duration)

if inPosition == False:

priceDeviation = mainPriceDeviation

safetyOrderSize = mainSafetyOrderSize

# LONG ENTER

if firstPrice - (firstPrice/100) * priceDeviation >= currentPrice and shortPosition == False and maxSafetyTradesCount>tradeCount and float(free_balance["BTC"]) >= baseOrderSize and (positionSide == 1 or positionSide == 3):

if tradeCount == 0:

alinacak_miktar = (baseOrderSize * 1 ) / float(df["close"][len(df.index) - 1])

if tradeCount > 0:

alinacak_miktar = (safetyOrderSize * 1 ) / float(df["close"][len(df.index) - 1])

safetyOrderSize = safetyOrderSize*safetyOrderVolumeScale

priceDeviation = priceDeviation * safetyOrderStepScale

longEnter(alinacak_miktar)

print("LONG ENTER")

first = True

tradeCount = tradeCount + 1

# SHORT ENTER

if ((firstPrice / 100) * priceDeviation) + firstPrice <= currentPrice and longPosition == False and maxSafetyTradesCount>tradeCount and float(free_balance["BTC"]) >= baseOrderSize and (positionSide == 2 or positionSide == 3):

if tradeCount == 0:

alinacak_miktar = (baseOrderSize * 1 ) / float(df["close"][len(df.index) - 1])

if tradeCount > 0:

alinacak_miktar = (safetyOrderSize * 1 ) / float(df["close"][len(df.index) - 1])

safetyOrderSize = safetyOrderSize*safetyOrderVolumeScale

priceDeviation = priceDeviation * safetyOrderStepScale

shortEnter(alinacak_miktar)

print("SHORT ENTER")

first = True

tradeCount = tradeCount + 1

# LONG TAKE PROFIT

if longPosition and ((float(position_info["entryPrice"][len(position_info.index) - 1])/100)*takeProfit)+float(position_info["entryPrice"][len(position_info.index) - 1]) < currentPrice and (positionSide == 1 or positionSide == 3):

print("TAKE PROFIT")

longExit()

first = True

tradeCount = 0

# SHORT TAKE PROFIT

if shortPosition and float(position_info["entryPrice"][len(position_info.index) - 1]) - (float(position_info["entryPrice"][len(position_info.index) - 1])/100) * takeProfit >= currentPrice and (positionSide == 2 or positionSide == 3):

print("TAKE PROFIT")

shortExit()

first = True

tradeCount = 0

# LONG STOP LOSS

if longPosition and (float(free_balance["BTC"]) <= baseOrderSize or maxSafetyTradesCount<=tradeCount) and firstPrice - (firstPrice/100) * stopLoss >= currentPrice and (positionSide == 1 or positionSide == 3):

print("STOP LOSS")

longExit()

first = True

tradeCount = 0

# SHORT STOP LOSS

if shortPosition and (float(free_balance["BTC"]) <= baseOrderSize or maxSafetyTradesCount<=tradeCount) and ((firstPrice / 100) * stopLoss) + firstPrice <= currentPrice and (positionSide == 2 or positionSide == 3):

print("STOP LOSS")

shortExit()

first = True

tradeCount = 0

if longPosition:

print("In Long Position")

if shortPosition:

print("In Short Position")

if inPosition:

print("Trade Count: ", tradeCount, " Avarege Price: ", float(position_info["entryPrice"][len(position_info.index) - 1]), " Free btc ", round(float(free_balance["BTC"]),2), " Total Money: ", round(float(balance['total']["BTC"]),2))

if inPosition == False:

print("Starting Price: ", firstPrice, " Current Price: ", currentPrice, " Total Money: ", round(float(balance['total']["BTC"]),2))

print("=======================================================================================================================================")

except ccxt.BaseError as Error:

print ("[ERROR] ", Error )

continue回答 1

Stack Overflow用户

发布于 2022-02-16 17:20:02

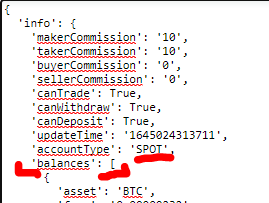

上面的图片是运行适用于(由ccxt库包装)的方法.fetch_balance()的结果。它是JSON格式的,我相信它不是

positions = balance['info']['positions']你应该试试

positions = balance['info']['balances']我不能保证,如果这将通过,其余的代码将工作,因为期货是不同的地方,我不熟悉期货。

页面原文内容由Stack Overflow提供。腾讯云小微IT领域专用引擎提供翻译支持

原文链接:

https://stackoverflow.com/questions/71057841

复制相关文章

相似问题

腾讯云开发者